Introduction

Starting a small business in Canada takes more than just a great idea—it demands thoughtful financial planning. A key decision is figuring out how to secure the funding you need. While self-funding might work initially, opening a business bank account and exploring external financing can drive growth and unlock new opportunities. This guide provides practical advice on navigating business loans in Canada, helping you make informed decisions for your startup’s financial success.

Key Highlights

- Variety of Loan Options: Discover different types of business loans available for Canadian startups, each designed with specific terms and eligibility requirements.

- Plan Your Finances: Before seeking funding, determine your required loan amount, considering your startup’s financial needs and ability to repay.

- CSBFP Advantages: The Canada Small Business Financing Program (CSBFP) can be a valuable resource, offering government-backed loans with favorable terms.

- Strong Application: Prepare a compelling loan application package, including a robust business plan, financial projections, and relevant documentation.

- Shop Around and Compare: Don’t settle for the first offer! Compare interest rates, terms, and conditions from different lenders to find the best fit for your startup.

Understanding Different Types of Business Loans in Canada

Selecting the right business loan is crucial for the growth of any startup. Understanding the various loan options available in Canada is essential, as each comes with its own interest rates, repayment terms, and eligibility requirements. Choosing a loan that aligns with your business’s specific needs can make all the difference.

If you need to buy equipment, raise working capital, or spend money on marketing, the right type of loan can help you a lot. Let’s take a look at two popular choices for startups: term loans and lines of credit.

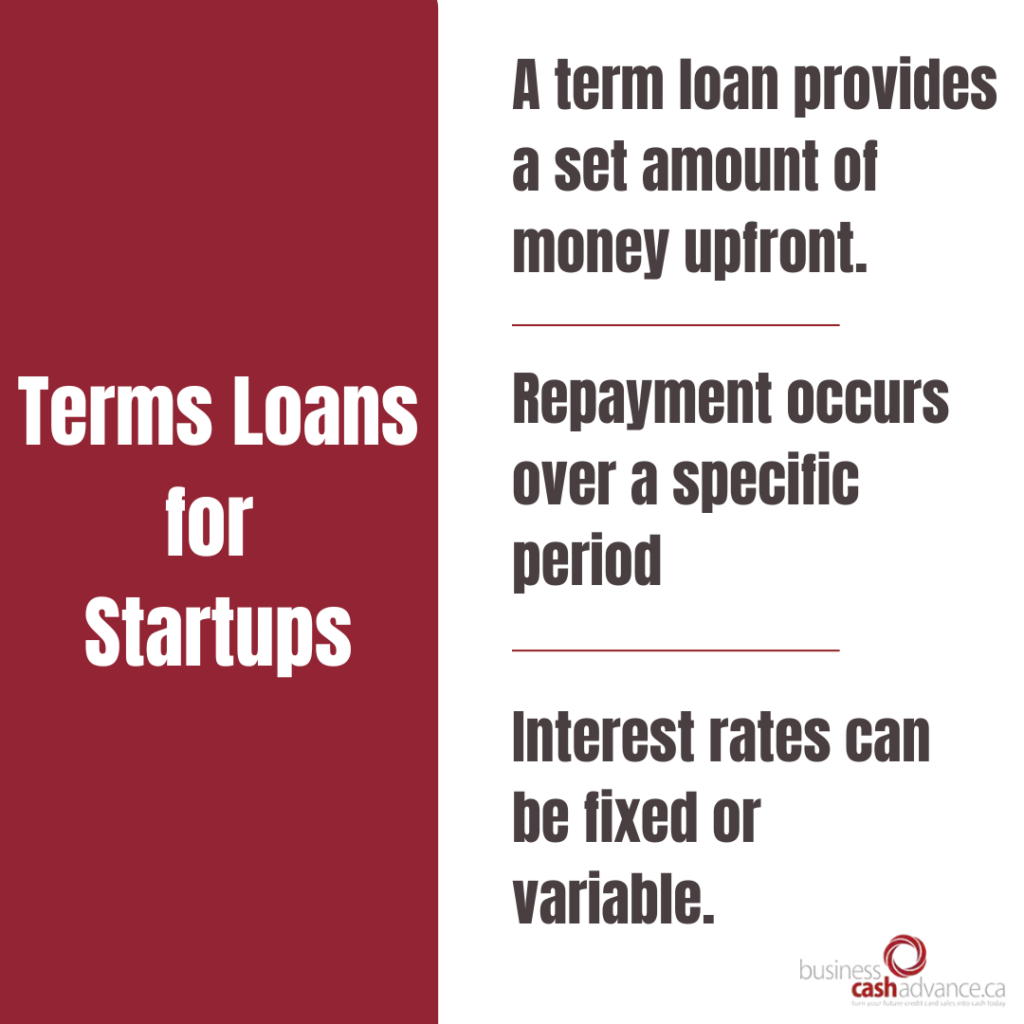

The Essentials of Term Loans for Startups

A term loan gives you a lump sum of money all at once. You pay this back over a specific time, and it can have either fixed or variable interest rates. This type of loan is good for big expenses, like buying equipment, acquiring real estate, or supporting large projects. The maximum loan amount can change based on the lender and your startup’s financial health.

One key benefit of term loans is that they have regular repayment plans. This makes it easier to manage your finances. But remember, the full loan balance starts to rack up interest from the day you receive it, no matter how you use the money.

So, it’s best to borrow only what you truly need. Make sure you have a strong plan for repayment to avoid extra interest fees.

Revolving Lines of Credit: What You Need to Know

A line of credit is different from a term loan. It allows you to use money up to a limit that has been approved ahead of time. You can borrow money, pay it back, and borrow again whenever you need to. This makes it great for keeping track of cash flow, paying for running costs, or taking care of unexpected bills.

Interest rates for lines of credit usually change and can be higher than rates for term loans. The good news is that you only pay interest on the money you actually use, giving you more financial freedom.

When picking a line of credit, it’s important to check and compare interest rates and fees from various banks to get the best deal. Also, keep in mind that using your credit wisely and paying on time can help improve your credit score, which could lead to better financing options for you in the future.

Evaluating Your Startup’s Financial Needs

Before approaching potential lenders, it’s crucial to understand your startup’s financial situation and determine the loan amount that suits your needs. Assess your finances by identifying key expenses such as purchasing equipment, covering operational costs, and allocating funds for marketing.

Thoroughly understanding your financial situation will help make your loan application easier. It will also show lenders that you can be a good borrower who has a clear plan for the future.

Estimating the Amount You Need to Borrow

Estimating how much money you need to borrow is very important for a small business seeking financing. First, think about how much money you need now and how much you’ll need in the future. This includes one-time costs like buying equipment and regular costs like payroll and rent. Look at your expected gross annual revenues and figure out your cash flow for each month or quarter.

This process helps identify potential cash shortfalls that may require external financing. Once you understand your income and expenses, calculate the funding gap you need to address. Be sure to account for unexpected costs by setting aside extra funds for unforeseen challenges. By carefully estimating your borrowing needs, you can avoid overburdening your business with debt and create a repayment plan that’s manageable and sustainable.

Planning for Repayment: Terms and Conditions

A crucial aspect of securing a business loan is understanding its repayment terms and conditions. Before signing any agreement, carefully review the lender’s terms, including the interest rate, repayment period, and any associated fees. Pay close attention to the fine print, such as prepayment penalties or conditions for default.

Consider your projected cash flow and ensure that your business can comfortably handle the monthly or quarterly repayments. It’s advisable to create a detailed repayment plan, outlining your repayment schedule and any contingencies.

Remember, responsible repayment not only fulfills your loan obligations but also builds a strong credit history, paving the way for favorable financing options.

| Feature | Term Loan | Line of Credit |

| Repayment | Fixed monthly or quarterly | Flexible, interest on usage |

| Interest | Fixed or variable | Typically variable |

| Access | Lump-sum upfront | Revolving, up to credit limit |

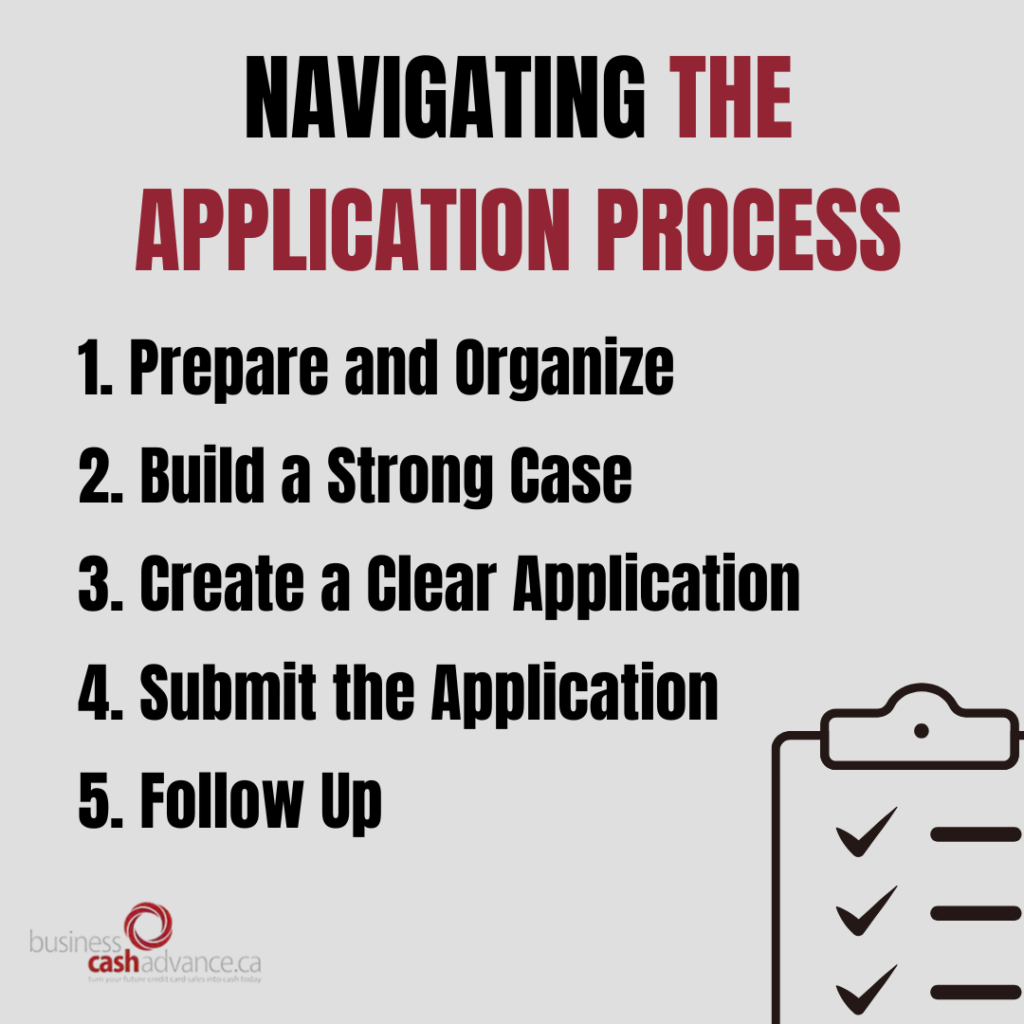

Navigating the Application Process

To apply for a business loan, you need to be organized. Make sure you present a strong case to the lenders. First, collect all the documents you need. This includes financial statements, tax returns, and a complete business plan. Highlight your startup’s strengths and the market opportunities available. Also, mention your team’s skills and strengths.

A clear and simple application shows that you are ready and honest. This can help improve your chances of getting approved.

Documents Required for Loan Application

Lenders usually ask for a lot of documents when reviewing your loan application. First, you must prepare a detailed business plan. The plan should share your startup’s vision, target market, competitive analysis, and financial forecasts.

You will also need to provide financial statements, like income statements, balance sheets, and cash flow statements. These show the financial health of your business.

Also, personal and business tax returns are often needed. They help show your financial history and that you have followed tax rules.

Depending on the loan type and amount applied for, lenders might ask for extra documents. This could include personal and business credit reports, proof of collateral, like real property or intangible assets, and legal documents, like articles of incorporation.

If you gather these documents in advance, it will make the application process smoother and help avoid delays.

Tips to Improve Your Chances of Approval

To increase your chances of securing a loan, maintain a strong credit score for both personal and business finances. Pay your bills on time and handle your debt wisely. Make a strong business plan that shows how your startup can succeed.

Explore government loan programs such as the Canada Small Business Financing Program (CSBFP), which often have more flexible qualification requirements and are offered through various banks. Additionally, consider alternative lenders like the Business Development Bank of Canada (BDC), which specializes in supporting small businesses.

Connect with your local Economic Development Canada (EDC) office. They can offer helpful resources and advice for new business owners. Showing that you manage your finances well and have a clear plan can help you get the funding you need.

Conclusion

When selecting a business loan for your Canadian startup, carefully evaluate your options based on your financial needs. Understand the types of loans available and determine how much funding you require. Consider your repayment plan to ensure it aligns with your business’s financial capacity.

Familiarize yourself with the application process to make it as smooth as possible. Stay informed about key requirements such as the minimum credit score, processing times, available government grants, revenue thresholds, and whether collateral is needed. This knowledge will simplify the application process and help you secure the right funding.

Making informed decisions will set your startup on the path to success.